Food Allergy Market Synopsis

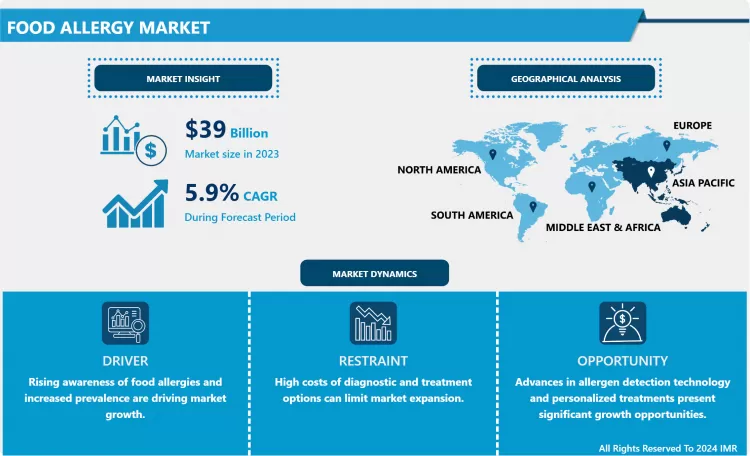

Food Allergy Market Size is Valued at USD 39.0 Billion in 2023, and is Projected to Reach USD 61.8 Billion by 2032, Growing at a CAGR of 5.9% From 2024-2032.

The food allergy market is rapidly growing due to increasing awareness and diagnosis of food allergies across all age groups. Factors such as the rising prevalence of allergic conditions, heightened awareness among consumers, and advances in diagnostic technologies are driving market expansion. The market includes a range of products, from allergen-free food alternatives to specialized testing and treatment solutions. Challenges include the need for stringent labelling regulations and managing cross-contamination risks. However, opportunities abound in developing innovative allergen-free products and personalized treatment approaches. As the global awareness of food allergies continues to rise, the market is poised for significant growth and innovation.

- The food allergy market is experiencing growth as consumers and healthcare professionals become more cognizant of food allergies and sensitivities. This market encompasses allergen-free food products, medical remedies, and allergy tests, all of which are associated with the diagnosis, treatment, and management of food allergies.

- Environmental changes and dietary habits are influencing the increasing prevalence of food allergies, driving the demand for innovative solutions tailored to the needs of those affected. Furthermore, regulatory advancements and increased research are facilitating the development of new and effective products to manage and prevent allergic reactions.

- The market is witnessing a notable surge in the introduction of hypoallergenic and allergen-free food products, aimed at satisfying the growing consumer demand for safe and health-conscious options. Technological advancements in food processing and diagnostics are improving the capacity to detect and manage allergies.

- However, obstacles like the complexity of regulatory requirements and the exorbitant cost of products can influence market growth. Despite these challenges, we anticipate the food allergy market to experience ongoing development and innovation due to the growing awareness of food allergies and the emphasis on personalized healthcare.

Food Allergy Market Trend Analysis

Increased Awareness and Diagnostic Advancements

- Increased awareness and advancements in diagnostic technologies are driving the food allergy market's significant growth. As the public becomes more aware of food allergies, there is a growing demand for specialized tests and remedies, as more people seek accurate diagnoses and effective management strategies.

- Innovative products specifically designed to accommodate individuals with food allergies are emerging as a result of this increased awareness, along with improved education on allergen avoidance. As a result, the market is expanding to encompass a broader selection of therapeutic solutions and diagnostic instruments.

- Advances in diagnostic technologies, such as allergen-specific immunoassays and molecular techniques, are revolutionizing the food allergy landscape. These advancements facilitate personalized treatment plans and improve patient outcomes by allowing for more precise and earlier detection of food allergies.

- We anticipate that the integration of these advanced diagnostic tools into routine clinical practice will further drive market growth, as healthcare providers and patients increasingly rely on these cutting-edge solutions to effectively manage food allergies.

Expansion of Allergen-Free and Specialized Products

- A growing awareness of food allergies and intolerances is driving a significant transition in the food allergy market toward allergen-free and specialized products. There is a growing demand among consumers for foods that are devoid of common allergens, including dairy, gluten, and nuts.

- This trend is motivating manufacturers to implement innovative strategies and create allergen-free alternatives that satisfy rigorous safety regulations while simultaneously offering nutritional benefits. As a result, the availability of specialized products, specifically designed to meet the needs of individuals with food allergies, has significantly increased, ensuring their access to safe and enjoyable dietary options.

- Growing regulatory support for allergen labeling and safety measures, along with advancements in food technology, are driving the sector's expansion. Companies are investing in research and development to improve production processes and create new formulations. Increased consumer awareness and advocacy, which drive demand for allergen-free foods and contribute to the overall growth of the food allergy market, further bolster the market's expansion.

Food Allergy Market Segment Analysis:

Food Allergy Market Segmented on the basis of By Diagnosis, By Symptoms, and By Food Source.

By Diagnosis, Elimination Diet segment is expected to dominate the market during the forecast period

- In the food allergy market, diagnostic methods are critical for the precise identification and management of allergic reactions. Elimination diets, which involve the removal of suspected allergens from the diet to identify triggers, continue to be a fundamental approach, particularly for the identification of food sensitivities.

- Skin-prick tests involve exposing the skin to potential allergens and observing reactions, whereas blood tests measure specific IgE antibodies to pinpoint allergens. The gold standard, oral food challenges, involves consuming the suspected allergen under medical supervision to confirm allergies. Newer, emerging technologies and patch testing are potential alternative diagnostic methods.

- The increasing prevalence of food allergies and the growing awareness of their management are stimulating the food allergy market. The market is expanding as a result of increased research into novel allergens and advancements in diagnostic technologies.

- Nevertheless, obstacles such as the necessity for personalized approaches and the variability in diagnostic accuracy may influence market growth. We anticipate that advancements in diagnostic methods and increased healthcare accessibility will improve market dynamics and patient outcomes.

By Symptoms, Atopic Dermatitis segment held the largest share in 2023

- The prevalence and severity of symptoms experienced by individuals influence key categories of the food allergy market, such as anaphylaxis, atopic dermatitis, and other allergic reactions. Atopic dermatitis, or chronic skin inflammation and irritation, is frequently associated with food allergies, particularly in children.

- Foods like crustaceans, nuts, or dairy frequently precipitate anaphylaxis, a severe, life-threatening reaction that necessitates immediate medical intervention. These symptoms have a significant impact on patient's quality of life and drive the demand for effective treatments and preventive measures.

- The market is experiencing growth as a result of a rise in allergy cases worldwide, enhanced diagnostic methods, and increased awareness. The management of these conditions is contingent upon the development of innovative diagnostic instruments and therapies.

- Additionally, consumers' increasing awareness of food allergies and the development of allergen-free food products position the market for expansion. This is due to healthcare providers and companies' efforts to cater to the diverse needs of individuals with food allergies.

Food Allergy Market Regional Insights:

Asia-Pacific to witness the highest growth during the assessment period

- During the assessment period, we anticipate the food allergy market to expand at the most rapid pace in the Asia-Pacific region. The increasing prevalence of allergic conditions, growing awareness of food allergies, and the enhancement of healthcare infrastructure in countries throughout the region fuel this expansion. Urbanization and dietary changes are also contributing to a heightened emphasis on food safety and allergy management, which is driving market expansion.

- In this ever-changing environment, we anticipate substantial progress in the food allergy market in the areas of diagnostic instruments, treatment options, and preventive measures. We anticipate innovations in allergen detection and personalized therapies to meet the increasing consumer demand for effective solutions.

- As the region continues to develop economically and healthcare systems advance, we expect the food allergy market to benefit from increased investment and research, leading to improved outcomes for individuals affected by food allergies.

Active Key Players in the Food Allergy Market

- Akorn, Incorporated (US)

- Pfizer Inc. (US)

- GlaxoSmithKline plc (UK)

- Novartis AG (Switzerland)

- Mylan N.V. (US)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sanofi (France)

- Boehringer Ingelheim International GmbH. (Germany)

- AstraZeneca (UK)

- Johnson & Johnson Private Limited (US)

- Bayer AG (Germany)

- Merck & Co., Inc. (US)

- Prestige Consumer Healthcare Inc. (US)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Bristol-Myers Squibb Company (US)

- Almirall, S.A (Spain)

- Zenomed Healthcare Private Limited (India)

- Cadila Pharmaceuticals (India)

- Astellas Pharma Inc. (Japan)

- Eli Lilly and Company (US), Other Active Players

Chapter 1: Introduction

1.1 Research Objectives

1.2 Research Methodology

1.3 Research Process

1.4 Scope and Coverage

1.4.1 Market Definition

1.4.2 Key Questions Answered

1.5 Market Segmentation

Chapter 2:Executive Summary

Chapter 3:Growth Opportunities By Segment

3.1 By Food Source

3.2 By Symptoms

3.3 By Treatment

3.4 By End User

3.5 By Distribution Channel

Chapter 4: Market Landscape

4.1 Porter's Five Forces Analysis

4.1.1 Bargaining Power of Supplier

4.1.2 Threat of New Entrants

4.1.3 Threat of Substitutes

4.1.4 Competitive Rivalry

4.1.5 Bargaining Power Among Buyers

4.2 Industry Value Chain Analysis

4.3 Market Dynamics

4.3.1 Drivers

4.3.2 Restraints

4.3.3 Opportunities

4.5.4 Challenges

4.4 Pestle Analysis

4.5 Technological Roadmap

4.6 Regulatory Landscape

4.7 SWOT Analysis

4.8 Price Trend Analysis

4.9 Patent Analysis

4.10 Analysis of the Impact of Covid-19

4.10.1 Impact on the Overall Market

4.10.2 Impact on the Supply Chain

4.10.3 Impact on the Key Manufacturers

4.10.4 Impact on the Pricing

Chapter 5: Food Allergy Market by Food Source

5.1 Food Allergy Market Overview Snapshot and Growth Engine

5.2 Food Allergy Market Overview

5.3 Crustacean shellfish

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size (2016-2028F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Crustacean shellfish: Geographic Segmentation

5.4 Dairy Products

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size (2016-2028F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Dairy Products: Geographic Segmentation

5.5 Poultry Products

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size (2016-2028F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 Poultry Products: Geographic Segmentation

5.6 Wheat

5.6.1 Introduction and Market Overview

5.6.2 Historic and Forecasted Market Size (2016-2028F)

5.6.3 Key Market Trends, Growth Factors and Opportunities

5.6.4 Wheat: Geographic Segmentation

5.7 Soybeans

5.7.1 Introduction and Market Overview

5.7.2 Historic and Forecasted Market Size (2016-2028F)

5.7.3 Key Market Trends, Growth Factors and Opportunities

5.7.4 Soybeans: Geographic Segmentation

5.8 Tree Nuts

5.8.1 Introduction and Market Overview

5.8.2 Historic and Forecasted Market Size (2016-2028F)

5.8.3 Key Market Trends, Growth Factors and Opportunities

5.8.4 Tree Nuts: Geographic Segmentation

5.9 Peanuts

5.9.1 Introduction and Market Overview

5.9.2 Historic and Forecasted Market Size (2016-2028F)

5.9.3 Key Market Trends, Growth Factors and Opportunities

5.9.4 Peanuts: Geographic Segmentation

5.10 Others

5.10.1 Introduction and Market Overview

5.10.2 Historic and Forecasted Market Size (2016-2028F)

5.10.3 Key Market Trends, Growth Factors and Opportunities

5.10.4 Others: Geographic Segmentation

Chapter 6: Food Allergy Market by Symptoms

6.1 Food Allergy Market Overview Snapshot and Growth Engine

6.2 Food Allergy Market Overview

6.3 Anaphylaxis

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size (2016-2028F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Anaphylaxis: Geographic Segmentation

6.4 Hives

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size (2016-2028F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Hives: Geographic Segmentation

6.5 Atopic Dermatitis

6.5.1 Introduction and Market Overview

6.5.2 Historic and Forecasted Market Size (2016-2028F)

6.5.3 Key Market Trends, Growth Factors and Opportunities

6.5.4 Atopic Dermatitis: Geographic Segmentation

6.6 Wheezing

6.6.1 Introduction and Market Overview

6.6.2 Historic and Forecasted Market Size (2016-2028F)

6.6.3 Key Market Trends, Growth Factors and Opportunities

6.6.4 Wheezing: Geographic Segmentation

6.7 Others

6.7.1 Introduction and Market Overview

6.7.2 Historic and Forecasted Market Size (2016-2028F)

6.7.3 Key Market Trends, Growth Factors and Opportunities

6.7.4 Others: Geographic Segmentation

Chapter 7: Food Allergy Market by Treatment

7.1 Food Allergy Market Overview Snapshot and Growth Engine

7.2 Food Allergy Market Overview

7.3 Epinephrine injection

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size (2016-2028F)

7.3.3 Key Market Trends, Growth Factors and Opportunities

7.3.4 Epinephrine injection: Geographic Segmentation

7.4 Oral Immunotherapy (OIT)

7.4.1 Introduction and Market Overview

7.4.2 Historic and Forecasted Market Size (2016-2028F)

7.4.3 Key Market Trends, Growth Factors and Opportunities

7.4.4 Oral Immunotherapy (OIT): Geographic Segmentation

7.5 Epicutaneous Immunotherapy (EPIT)

7.5.1 Introduction and Market Overview

7.5.2 Historic and Forecasted Market Size (2016-2028F)

7.5.3 Key Market Trends, Growth Factors and Opportunities

7.5.4 Epicutaneous Immunotherapy (EPIT): Geographic Segmentation

7.6 Antihistamines

7.6.1 Introduction and Market Overview

7.6.2 Historic and Forecasted Market Size (2016-2028F)

7.6.3 Key Market Trends, Growth Factors and Opportunities

7.6.4 Antihistamines: Geographic Segmentation

7.7 Others

7.7.1 Introduction and Market Overview

7.7.2 Historic and Forecasted Market Size (2016-2028F)

7.7.3 Key Market Trends, Growth Factors and Opportunities

7.7.4 Others: Geographic Segmentation

Chapter 8: Food Allergy Market by End User

8.1 Food Allergy Market Overview Snapshot and Growth Engine

8.2 Food Allergy Market Overview

8.3 Hospitals

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size (2016-2028F)

8.3.3 Key Market Trends, Growth Factors and Opportunities

8.3.4 Hospitals: Geographic Segmentation

8.4 Specialty Clinics

8.4.1 Introduction and Market Overview

8.4.2 Historic and Forecasted Market Size (2016-2028F)

8.4.3 Key Market Trends, Growth Factors and Opportunities

8.4.4 Specialty Clinics: Geographic Segmentation

8.5 Individuals

8.5.1 Introduction and Market Overview

8.5.2 Historic and Forecasted Market Size (2016-2028F)

8.5.3 Key Market Trends, Growth Factors and Opportunities

8.5.4 Individuals: Geographic Segmentation

8.6 Others

8.6.1 Introduction and Market Overview

8.6.2 Historic and Forecasted Market Size (2016-2028F)

8.6.3 Key Market Trends, Growth Factors and Opportunities

8.6.4 Others: Geographic Segmentation

Chapter 9: Food Allergy Market by Distribution Channel

9.1 Food Allergy Market Overview Snapshot and Growth Engine

9.2 Food Allergy Market Overview

9.3 Hospital Pharmacy

9.3.1 Introduction and Market Overview

9.3.2 Historic and Forecasted Market Size (2016-2028F)

9.3.3 Key Market Trends, Growth Factors and Opportunities

9.3.4 Hospital Pharmacy: Geographic Segmentation

9.4 Retail Pharmacy

9.4.1 Introduction and Market Overview

9.4.2 Historic and Forecasted Market Size (2016-2028F)

9.4.3 Key Market Trends, Growth Factors and Opportunities

9.4.4 Retail Pharmacy: Geographic Segmentation

9.5 Online Pharmacy

9.5.1 Introduction and Market Overview

9.5.2 Historic and Forecasted Market Size (2016-2028F)

9.5.3 Key Market Trends, Growth Factors and Opportunities

9.5.4 Online Pharmacy: Geographic Segmentation

Chapter 10: Company Profiles and Competitive Analysis

10.1 Competitive Landscape

10.1.1 Competitive Positioning

10.1.2 Food Allergy Sales and Market Share By Players

10.1.3 Industry BCG Matrix

10.1.4 Heat Map Analysis

10.1.5 Food Allergy Industry Concentration Ratio (CR5 and HHI)

10.1.6 Top 5 Food Allergy Players Market Share

10.1.7 Mergers and Acquisitions

10.1.8 Business Strategies By Top Players

10.2 BOEHRINGER INGELHEIM INTERNATIONAL GMBH. (GERMANY)

10.2.1 Company Overview

10.2.2 Key Executives

10.2.3 Company Snapshot

10.2.4 Operating Business Segments

10.2.5 Product Portfolio

10.2.6 Business Performance

10.2.7 Key Strategic Moves and Recent Developments

10.2.8 SWOT Analysis

10.3 AIMMUNE THERAPEUTICS INC (USA)

10.4 JOHNSON & JOHNSON PRIVATE LIMITED (USA)

10.5 MERCK & CO. INC. (US)

10.6 PRESTIGE CONSUMER HEALTHCARE INC. (US)

10.7 BAYER AG (GERMANY)

10.8 ASTRAZENECA (UK)

10.9 DBV TECHNOLOGIES (FRANCE)

10.10 NOVARTIS PHARMACEUTICALS (SWITZERLAND)

10.11 F. HOFFMANN-LA ROCHE LTD. (SWITZERLAND)

10.12 ALLADAPT IMMUNOTHERAPEUTICS (USA)

10.13 VEDANTA BIOSCIENCES INC (USA)

10.14 ALLADAPT IMMUNOTHERAPEUTICS (USA)

10.15 ALMIRALL S.A (SPAIN)

10.16 SANOFI (FRANCE)

10.17 PFIZER INC (USA)

10.18 OTHER MAJOR PLAYERS

Chapter 11: Global Food Allergy Market Analysis, Insights and Forecast, 2016-2028

11.1 Market Overview

11.2 Historic and Forecasted Market Size By Food Source

11.2.1 Crustacean shellfish

11.2.2 Dairy Products

11.2.3 Poultry Products

11.2.4 Wheat

11.2.5 Soybeans

11.2.6 Tree Nuts

11.2.7 Peanuts

11.2.8 Others

11.3 Historic and Forecasted Market Size By Symptoms

11.3.1 Anaphylaxis

11.3.2 Hives

11.3.3 Atopic Dermatitis

11.3.4 Wheezing

11.3.5 Others

11.4 Historic and Forecasted Market Size By Treatment

11.4.1 Epinephrine injection

11.4.2 Oral Immunotherapy (OIT)

11.4.3 Epicutaneous Immunotherapy (EPIT)

11.4.4 Antihistamines

11.4.5 Others

11.5 Historic and Forecasted Market Size By End User

11.5.1 Hospitals

11.5.2 Specialty Clinics

11.5.3 Individuals

11.5.4 Others

11.6 Historic and Forecasted Market Size By Distribution Channel

11.6.1 Hospital Pharmacy

11.6.2 Retail Pharmacy

11.6.3 Online Pharmacy

Chapter 12: North America Food Allergy Market Analysis, Insights and Forecast, 2016-2028

12.1 Key Market Trends, Growth Factors and Opportunities

12.2 Impact of Covid-19

12.3 Key Players

12.4 Key Market Trends, Growth Factors and Opportunities

12.4 Historic and Forecasted Market Size By Food Source

12.4.1 Crustacean shellfish

12.4.2 Dairy Products

12.4.3 Poultry Products

12.4.4 Wheat

12.4.5 Soybeans

12.4.6 Tree Nuts

12.4.7 Peanuts

12.4.8 Others

12.5 Historic and Forecasted Market Size By Symptoms

12.5.1 Anaphylaxis

12.5.2 Hives

12.5.3 Atopic Dermatitis

12.5.4 Wheezing

12.5.5 Others

12.6 Historic and Forecasted Market Size By Treatment

12.6.1 Epinephrine injection

12.6.2 Oral Immunotherapy (OIT)

12.6.3 Epicutaneous Immunotherapy (EPIT)

12.6.4 Antihistamines

12.6.5 Others

12.7 Historic and Forecasted Market Size By End User

12.7.1 Hospitals

12.7.2 Specialty Clinics

12.7.3 Individuals

12.7.4 Others

12.8 Historic and Forecasted Market Size By Distribution Channel

12.8.1 Hospital Pharmacy

12.8.2 Retail Pharmacy

12.8.3 Online Pharmacy

12.9 Historic and Forecast Market Size by Country

12.9.1 U.S.

12.9.2 Canada

12.9.3 Mexico

Chapter 13: Europe Food Allergy Market Analysis, Insights and Forecast, 2016-2028

13.1 Key Market Trends, Growth Factors and Opportunities

13.2 Impact of Covid-19

13.3 Key Players

13.4 Key Market Trends, Growth Factors and Opportunities

13.4 Historic and Forecasted Market Size By Food Source

13.4.1 Crustacean shellfish

13.4.2 Dairy Products

13.4.3 Poultry Products

13.4.4 Wheat

13.4.5 Soybeans

13.4.6 Tree Nuts

13.4.7 Peanuts

13.4.8 Others

13.5 Historic and Forecasted Market Size By Symptoms

13.5.1 Anaphylaxis

13.5.2 Hives

13.5.3 Atopic Dermatitis

13.5.4 Wheezing

13.5.5 Others

13.6 Historic and Forecasted Market Size By Treatment

13.6.1 Epinephrine injection

13.6.2 Oral Immunotherapy (OIT)

13.6.3 Epicutaneous Immunotherapy (EPIT)

13.6.4 Antihistamines

13.6.5 Others

13.7 Historic and Forecasted Market Size By End User

13.7.1 Hospitals

13.7.2 Specialty Clinics

13.7.3 Individuals

13.7.4 Others

13.8 Historic and Forecasted Market Size By Distribution Channel

13.8.1 Hospital Pharmacy

13.8.2 Retail Pharmacy

13.8.3 Online Pharmacy

13.9 Historic and Forecast Market Size by Country

13.9.1 Germany

13.9.2 U.K.

13.9.3 France

13.9.4 Italy

13.9.5 Russia

13.9.6 Spain

13.9.7 Rest of Europe

Chapter 14: Asia-Pacific Food Allergy Market Analysis, Insights and Forecast, 2016-2028

14.1 Key Market Trends, Growth Factors and Opportunities

14.2 Impact of Covid-19

14.3 Key Players

14.4 Key Market Trends, Growth Factors and Opportunities

14.4 Historic and Forecasted Market Size By Food Source

14.4.1 Crustacean shellfish

14.4.2 Dairy Products

14.4.3 Poultry Products

14.4.4 Wheat

14.4.5 Soybeans

14.4.6 Tree Nuts

14.4.7 Peanuts

14.4.8 Others

14.5 Historic and Forecasted Market Size By Symptoms

14.5.1 Anaphylaxis

14.5.2 Hives

14.5.3 Atopic Dermatitis

14.5.4 Wheezing

14.5.5 Others

14.6 Historic and Forecasted Market Size By Treatment

14.6.1 Epinephrine injection

14.6.2 Oral Immunotherapy (OIT)

14.6.3 Epicutaneous Immunotherapy (EPIT)

14.6.4 Antihistamines

14.6.5 Others

14.7 Historic and Forecasted Market Size By End User

14.7.1 Hospitals

14.7.2 Specialty Clinics

14.7.3 Individuals

14.7.4 Others

14.8 Historic and Forecasted Market Size By Distribution Channel

14.8.1 Hospital Pharmacy

14.8.2 Retail Pharmacy

14.8.3 Online Pharmacy

14.9 Historic and Forecast Market Size by Country

14.9.1 China

14.9.2 India

14.9.3 Japan

14.9.4 Singapore

14.9.5 Australia

14.9.6 New Zealand

14.9.7 Rest of APAC

Chapter 15: Middle East & Africa Food Allergy Market Analysis, Insights and Forecast, 2016-2028

15.1 Key Market Trends, Growth Factors and Opportunities

15.2 Impact of Covid-19

15.3 Key Players

15.4 Key Market Trends, Growth Factors and Opportunities

15.4 Historic and Forecasted Market Size By Food Source

15.4.1 Crustacean shellfish

15.4.2 Dairy Products

15.4.3 Poultry Products

15.4.4 Wheat

15.4.5 Soybeans

15.4.6 Tree Nuts

15.4.7 Peanuts

15.4.8 Others

15.5 Historic and Forecasted Market Size By Symptoms

15.5.1 Anaphylaxis

15.5.2 Hives

15.5.3 Atopic Dermatitis

15.5.4 Wheezing

15.5.5 Others

15.6 Historic and Forecasted Market Size By Treatment

15.6.1 Epinephrine injection

15.6.2 Oral Immunotherapy (OIT)

15.6.3 Epicutaneous Immunotherapy (EPIT)

15.6.4 Antihistamines

15.6.5 Others

15.7 Historic and Forecasted Market Size By End User

15.7.1 Hospitals

15.7.2 Specialty Clinics

15.7.3 Individuals

15.7.4 Others

15.8 Historic and Forecasted Market Size By Distribution Channel

15.8.1 Hospital Pharmacy

15.8.2 Retail Pharmacy

15.8.3 Online Pharmacy

15.9 Historic and Forecast Market Size by Country

15.9.1 Turkey

15.9.2 Saudi Arabia

15.9.3 Iran

15.9.4 UAE

15.9.5 Africa

15.9.6 Rest of MEA

Chapter 16: South America Food Allergy Market Analysis, Insights and Forecast, 2016-2028

16.1 Key Market Trends, Growth Factors and Opportunities

16.2 Impact of Covid-19

16.3 Key Players

16.4 Key Market Trends, Growth Factors and Opportunities

16.4 Historic and Forecasted Market Size By Food Source

16.4.1 Crustacean shellfish

16.4.2 Dairy Products

16.4.3 Poultry Products

16.4.4 Wheat

16.4.5 Soybeans

16.4.6 Tree Nuts

16.4.7 Peanuts

16.4.8 Others

16.5 Historic and Forecasted Market Size By Symptoms

16.5.1 Anaphylaxis

16.5.2 Hives

16.5.3 Atopic Dermatitis

16.5.4 Wheezing

16.5.5 Others

16.6 Historic and Forecasted Market Size By Treatment

16.6.1 Epinephrine injection

16.6.2 Oral Immunotherapy (OIT)

16.6.3 Epicutaneous Immunotherapy (EPIT)

16.6.4 Antihistamines

16.6.5 Others

16.7 Historic and Forecasted Market Size By End User

16.7.1 Hospitals

16.7.2 Specialty Clinics

16.7.3 Individuals

16.7.4 Others

16.8 Historic and Forecasted Market Size By Distribution Channel

16.8.1 Hospital Pharmacy

16.8.2 Retail Pharmacy

16.8.3 Online Pharmacy

16.9 Historic and Forecast Market Size by Country

16.9.1 Brazil

16.9.2 Argentina

16.9.3 Rest of SA

Chapter 17 Investment Analysis

Chapter 18 Analyst Viewpoint and Conclusion

|

Global Food Allergy Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 39.0 Bn. |

|

Forecast Period 2024-32 CAGR: |

5.9% |

Market Size in 2032: |

USD 61.8 Bn. |

|

Segments Covered: |

By Diagnosis |

|

|

|

By Symptoms |

|

||

|

By Food Source |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Global Food Allergy Market research report is 2024-2032.

Akorn, Incorporated (US), Pfizer Inc. (US), GlaxoSmithKline plc (UK), Novartis AG (Switzerland), Mylan N.V. (US), Teva Pharmaceutical Industries Ltd. (Israel), Sanofi (France), Boehringer Ingelheim International GmbH. (Germany), AstraZeneca (UK), Johnson & Johnson Private Limited (US), Bayer AG (Germany), Merck & Co., Inc. (US), Prestige Consumer Healthcare Inc. (US), F. Hoffmann-La Roche Ltd. (Switzerland), Bristol-Myers Squibb Company (US), Almirall, S.A (Spain), Zenomed Healthcare Private Limited (India), Cadila Pharmaceuticals (India), Astellas Pharma Inc. (Japan), Eli Lilly and Company (US), others

The Food Allergy Market is segmented into By Diagnosis (Elimination Diet, Blood Test, Skin-Prick Tests, Oral Food Challenge, and Others), By Symptoms (Atopic Dermatitis, Anaphylaxis, and Others), By Food Source (Wheat, Soy, Poultry Products, Dairy Products, Shellfish, Peanuts, Tree Nuts, and Others). By region, it is analyzed across North America (U.S.; Canada; Mexico), Eastern Europe (Bulgaria; The Czech Republic; Hungary; Poland; Romania; Rest of Eastern Europe), Western Europe (Germany; UK; France; Netherlands; Italy; Russia; Spain; Rest of Western Europe), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

Specific proteins present in specific foods initiate adverse immune responses that characterize food allergies. These reactions can range from benign symptoms, such as hives, to severe anaphylactic reactions. Environmental changes, genetic predispositions, and dietary practices are all contributing to the increasing prevalence of food allergies worldwide. Improved diagnostic instruments and increased awareness are enabling more effective identification and management of these allergies. Innovations in immunotherapy, allergen detection, and hypoallergenic foods are providing new solutions to the growing market for food allergy treatments and products. Improvements to the quality of life for individuals with food allergies continue to be a top priority as healthcare systems and research continue to develop.

Food Allergy Market Size is Valued at USD 39.0 Billion in 2023 and is Projected to Reach USD 61.8 Billion by 2032, Growing at a CAGR of 5.9% From 2024-2032.